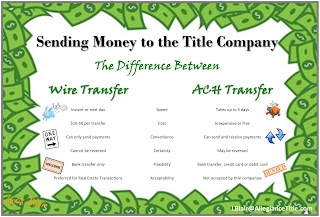

Not all money transfers are created equal. Both wire and Automated Clearing House (ACH) transfers are ways to electronically move money from one bank account to another. They may seem alike, but they are not.

These methods of sending funds are referred to as an EFT or electronic funds transfer. EFT is an umbrella expression that includes various types of financial transactions. EFT payments include wire transfers, ACH transfers, e-checks, ATMs, Point of Sale transactions, and more.

Understanding the differences between these is crucial when sending money to a title company.

Wire Transfer

Wire transfers are electronic payments used to send funds directly from one entity’s bank account to another’s. With wire payments, funds are instantly accessible when they arrive in the payee’s bank account and the recipient can access the funds without delay.

Wires are often used for large transactions when reliability and speed are critical factors. Because of the speed, once funds have been wired, reversing the transfer is difficult if not impossible.

Wire transfers can include a cost to both the sender and the recipient. Wire transfer fees are set by each financial institution and range from $10 to $100 to send or receive a wire transfer.

Title companies warn clients that wire transmissions are often the target of scams. It is essential to confirm the person and account that the funds are being sent to prior to initiating a wire transfer. Wire instructions will always include the bank routing number, account number, and name of the party receiving the money.

Wire transfers are preferred by title companies for security and dependability. They are much better than cashier’s checks, which can take longer to process and have become easy to counterfeit.

ACH Transfer

An Automated Clearinghouse transfer, or ACH, also moves money electronically. This is similar to sending a check and is becoming more common as a means to replace paper checks. ACH transfers may be the system used if you have automated bill payments, direct payroll deposits, or make direct person-to-person payments through PayPal, Venmo, or another system.

ACH payments are typically best for frequent or recurring transactions where the amount is smaller. Consumers like them for recurring payments for utilities, loans, etc., and for payments for services like Uber. Both large and small businesses like ACH as an e-payment method in this digital economy. Money can be both sent and received with ACH transfers.

The lower cost makes an ACH an appealing option for most consumers. Most ACH transfers are free for the sender or cost just a few dollars. While ACH payments are less expensive, wire transfers are faster.

The ACH network electronically processes transfers in large batches or groups to an automated clearinghouse, which sends them onto a bank. These can take a few hours or several days to complete and clear. The process is too slow for funding real estate transactions where time is of the essence. With a real estate sale, the closing is not complete and the property does not change ownership until all funds are confirmed and processed by the title company. ACH payments do not meet the definition of “good funds” per the Texas Insurance Code, Title XI, Section 2651.202. Sending the title company an ACH transfer for closing is a recipe for delays.

In addition to the time factor, title agents are averse to ACH transfers because they may be reversed. The criteria for stopping an ACH transfer is determined by each bank.

When purchasing a property, always confirm that funds sent to the title company are via a confirmed wire transfer and not an ACH transfer. If your Bank of America rep tells you they are the same thing, they are wrong. Follow the title company instructions and remember that the task of getting good funds to the title company on time is the responsibility of the buyer.

No comments:

Post a Comment