How much are closing costs? That depends. How nice are you to the title company? Just kidding.

Closing costs vary depending on the sales price, county, type of property (single family home, condo, raw land, etc.), and other factors that have nothing to do with how nice you play. Who pays the closing costs – buyer or seller — are sometimes mandated, sometimes standard practice, and sometimes can be negotiated. In Dallas, it is common, but not mandatory, for the seller to pay the broker commissions, prorated taxes, recording fee, escrow fees, tax certificate, document preparation costs, HOA transfer fees, resale certificate and other miscellaneous negotiable costs (like a home warranty or survey).

One of the large closing expenses is the title insurance premium. In Texas, title insurance rates are established by Texas Department of Insurance and all title companies must charge the same for title insurance. In other states, consumers often shop around for title insurance like they would for auto or home insurance.

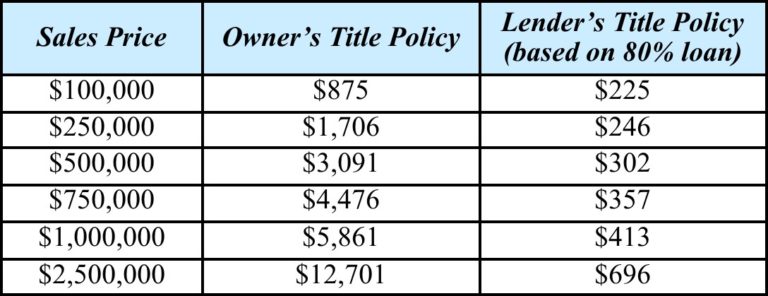

The following Title Insurance Basic Premium Rates are based on the sales price of the property. Premiums for policies $100,000 and over in Dallas County are:

Additionally, there are endorsements that can be added on to include coverage for survey deletion, leaseholds, condos, etc. Those are an additional charge. But the good news that unlike auto, home or health insurance, you pay this premium only once at closing. It’s not an ongoing cost like other types of insurance.

Title companies may charge different amounts for the closing costs outside of the title insurance policy. One may charge slightly more or less for the attorney review while another may charge more of less for the courier fees. But they are typically within a few dollars of each other when you look at the total costs.

It’s always a good idea to get title insurance and lenders require it to finance a purchase. Title insurance protects homebuyers from other claims of ownership, outstanding debts of previous owners, fraud, and other title potential problems. Before issuing a title insurance policy, the title company will check for problems with a title by researching public records, deeds, mortgages, wills, divorce decrees, court judgments, tax records, liens, encumbrances, etc. If there is a claim against your property after purchase, the company will defend you in court and will pay you for covered losses up to the amount of your policy.

Like any regulated service business, the difference between one title company and another comes down to service and reputation. If you’re not frequently selling a home, it’s unlikely you know which title companies offer the best service. That’s where a knowledgeable Realtor comes in. They generally can’t save you any money. But good agents have good relationships with title companies that can help make the process run smoothly.

[where: 75230]

No comments:

Post a Comment